BUY-BACK OF SHARES V/S DIVIDEND

A dividend offers cash rewards to all shareholders in accordance with their stake in the company, whereas a share buyback returns money only to those who decide to sell their shares.

This Article will talk about how buy back of shares is different from Dividend.

BUY-BACK OF SHARES V/S DIVIDEND

BUYBACK

Meaning of Buy-back:

With buy-back of shares, a company can purchase back some portion of its own stocks or specified securities. This is done by companies for various reasons like having too many floating stocks in the market, poor performance of the share prices, as well as to utilise any excess cash they have. Many times a company has excess cash on its balance sheet which it wants to distribute amongst its shareholders.

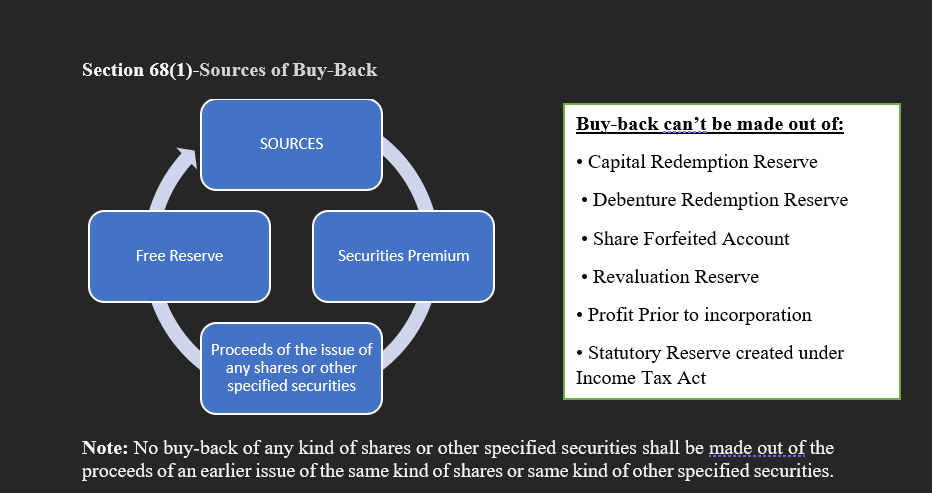

Meaning of Free Reserve:

As per Section 2(43) of the Companies Act, 2013: “free reserves” means such reserves which, as per the latest audited balance sheet of a company, are available for distribution as dividend.

For the purposes of section 68, “free reserves” includes securities premium account.

Meaning of Specified Securities:

For the purposes of section 68 and 70, “specified securities” includes employees’ stock option or other securities as may be notified by the Central Government from time to time.

No security has so far been notified as “specified securities”.

Objectives/Advantages of Buy-back of shares:

The following may be the objectives/advantages of buy-back of shares:

- To increase the promoters holding.

- To increase EPS.

- To pay surplus cash to the shareholders

- To reward shareholders by Buy-back of shares at much higher price than ruling market price.

- It safeguard against a hostile takeover by increasing promoters holding.

LEGAL FRAMEWORK:

Section 68, 69, and 70 of the Companies Act, 2013 (“the act”) read with Rule 17 of the Companies (Share Capital and Debentures) Rules, 2014 (“rule”).

CONDITIONS FOR BUY-BACK:

- Buy-back shall be authorized by the articles of association (AOA) of the Company;

- Board resolution shall be passed if Buy-back is 10% or less of the company’s total paid-up equity capital and free reserves;

- Special Resolution shall be passed if Buy-back is more than 10% of the company’s total paid-up equity capital and free reserves.

- Maximum Buyback’s limit:

- Through Board’s approval: 10% or less of the total paid-up equity capital and free reserves of the company;

- Through Shareholder’s approval: 25% or less of the aggregate of paid-up capital and free reserves of the company; and not more than 25% of total Paid-up Equity in that financial year

- Debt equity ratio post buy back should not exceed 2:1

- Only fully paid-up shares can be bought back

- No offer of buy-back under this sub-section shall be made within a period of 1 year from the date of the closure of the preceding offer of buy-back, if any.

- The notice of the meeting at which the special resolution is proposed to be passed under shall be accompanied by an explanatory statement stating—

(a) a full and complete disclosure of all material facts;

(b) the necessity for the buy-back;

(c) the class of shares or securities intended to be purchased under the buy-back.

(d) the amount to be invested under the buy-back; and

(e) the time-limit for completion of buy-back.

CHECK LIST FOR BUY-BACK OF SHARES

1. PRELIMINARY STEPS

- Before availing of the Buy-back facility, it’s important to check the Articles of Association (AoA). If it doesn’t specifically provide for the purchase of its own shares, the Company must take necessary steps to make amendments in the AoA. [Section 68(2)(a)]

- Determine the quantum of shares to be bought-back. [Section 68(2)(c)]

- The ratio of the aggregate of secured and unsecured debts owed by the company after buy-back should not exceed twice the paid-up capital and its free reserves. [Section 68(2)(d)].

- Only fully paid up shares can be buy-back. [Section 68(2)(e)]

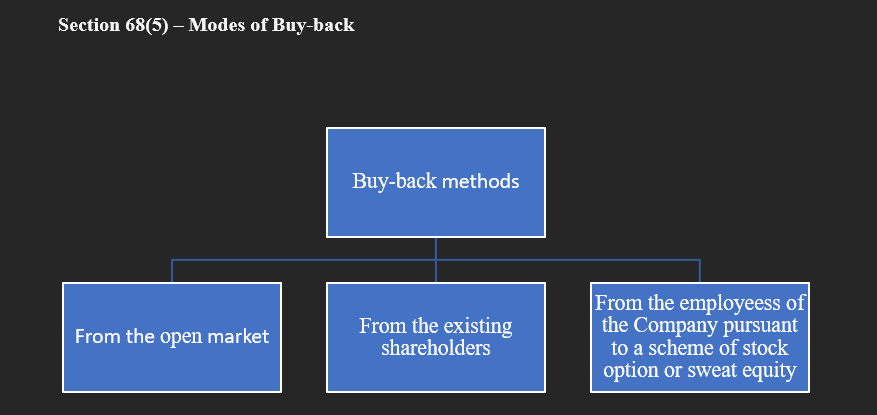

- Decide the quantum of the shares to be bought-back, the mode of purchase and the source of financing this purchase. :-

- From the existing shareholders or security holders on a proportionate basis

- From the open market

- By purchasing the securities issued to employees of the company pursuant to a scheme of stock option or sweat equity.

- Check there are no defaults subsisting in repayment of deposits, interest payment thereon, redemption of debentures or payment of interest thereon or redemption of preference shares or payment of dividend due to any shareholder, or repayment of any term loans or interest payable thereon to any financial institution or banking company. [Rule 17(1)(l)] of the Companies (Share Capital and Debentures) Rules, 2014 (“Rule”)]

- Every buy-back shall be completed within a period of 1 year from the date of passing of the board/special resolution, as the case may be.

2. BOARD FUNCTIONS

- Approve the quantum of shares to be purchased by the company and the price to be offered therefor.

- Decide on the period upto which the offer should be kept open.

- Decide whether the shares are to be bought-back out of free reserves, securities premium account or out of proceeds of the issue of any shares or other specified securities.

- Pass a Board Resolution approving the buy-back and convening a general meeting, if required, to consider and adopt special resolutions for altering the AoA where necessary and for the purchase of its own shares.

- Approve the draft notice convening the general meeting containing the above special resolutions and the draft of the explanatory statement to be annexed threreto. The board must make sure that the special resolution is transparent and contains the necessary disclosures and that the explanatory statement contains the material facts as are required under. The explanatory statement to be annexed to the notice of the general meeting pursuant to section 102 of the act shall contain the disclosures as required under Rule 17(1).

- The company shall complete the verifications of the offers received within 15 days from the date of closure of the offer and the shares or other securities lodged shall be deemed to be accepted unless a communication of rejection is made within 21 days from the date of closure of the offer.[Rule 17(7)]

3. General Meeting

(i) Pass special resolution to amend the AoA, if required

(ii) Pass another special resolution authorizing the Board to take steps to buy-back its shares and also to approve the explanatory statement annexed to the notice convening the meeting.

4. SECRETARIAL CHECK-LIST

- Convene a Board meeting to transact the business as set out in para 2 above and any other business.

- Convene a general meeting after giving due notice to transact the business as set out in para 3 above. Ensure that the explanatory statement contains all the disclosures and information as required under Rule 17(1) (a) of the Companies (Share Capital and Debentures) Rules, 2014 (“Rule”).

- File Form MGT-14 together with the Board/Special resolutions so passed along with the Notice and Explanatory statement with the Registrar of Companies within 30 days of passing of the said resolutions as required under section 179(3)(b).

- File letter of offer with the Registrar of companies in Form no. SH.8 and such letter of offer shall be dated and signed on behalf of the Board of directors of the company by not less than 2 directors of the company, one of whom shall be the managing director, if any. [Rule 17(2)].

- Ensure that the letter of offer is dispatched to the shareholders or security holders immediately after filing the same with the Registrar of Companies but not later than 20 days from its filing with the Registrar of Companies. [Rule 17(4)].

- File Declaration of Solvency in Form No. SH-9 along with the letter of offer in Form No. SH-8 with Registrar of Companies before commencing the buy-back of shares and shall ensure that [Rule 17(3)]:

- Such Declaration and Letter of Offer to be signed by at least two directors of the company, one of whom shall be the managing director, if any, and

- Such declaration to be verified by an affidavit to the effect that the Board of Directors of the company has made a full inquiry into the affairs of the Company as a result of which they have formed an opinion that it is capable of meeting its liabilities and will not be rendered insolvent within a period of one year from the date of declaration adopted by the Board:

- Make sure that the buy-back offer shall remain open for a minimum period of 15 days and not exceeding 30 days from the date of dispatch of letter of offer. Provided that where all members of a company agree, the offer for buy-back may remain open for a period less than 15 days [Rule 17(5)]

- Complete the verifications of the offers received within 15 days from the date of closure of the offer and the shares or other securities lodged shall be deemed to be accepted unless a communication of rejection is made within 21 days from the date of closure of the offer. [Rule 17(7)]

- Open a separate bank account immediately after closure of the offer and deposit therein, such sum, as would make up the entire sum due and payable as consideration for the shares tendered for buy-back. [Rule 17(8)]

- Where a company purchases its own shares out of free reserves or securities premium account, a sum equal to the nominal value of the shares so purchased shall be transferred to the capital redemption reserve account and details of such transfer shall be disclosed in the balance sheet.[Section 69(1)]

Monitor that the Company shall make payments to those shareholders or security holders whose securities have been accepted within 7 days of the time specified in sub-rule (7) of Rule 17; or

return the share certificates to the shareholders or security holders whose securities have not been accepted at all or the balance of securities in case of part acceptance. [Rule 17(9)]The company should extinguish and physically destroy the share certificates so bought-back within 7 days of the last date of completion of buy-back. [Section 68(7)]

The company, shall maintain a register of shares or other securities which have been bought-back in Form No. SH.10. [Section 68(9) and Rule 17((12)(a)]

The register of shares or securities bought-back shall be maintained at the registered office of the company and shall be kept in the custody of the secretary of the company or any other person authorized by the board in this behalf. [Rule 17(12)(b)]

The entries in the register shall be authenticated by the secretary of the company or by any other person authorized by the Board for the purpose. [Rule 17(12)(c)]File a Return of Buy- Back in Form No. SH-11 with the Registrar of Companies within 30 days of completion of Buy- Back. [Rule 17(13)]

The company while filling a return in Form No. SH-11 should annex a certificate in Form No. SH-15 duly signed by 2 Directors including the managing director, if any, certifying that the buy-back of securities has been made in compliance with the provisions of the Act and the rules made thereunder. [Rule 17 (14)]

Section 70 - Prohibition for Buy-Back in Certain Circumstances

No company shall directly or indirectly purchase its own shares or other specified securities—

a) through any subsidiary company including its own subsidiary companies;

b) through any investment company or group of investment companies; or

c) if a default, is made by the company, in the repayment of deposits accepted either before or after the commencement of this Act, interest payment thereon, redemption of debentures or preference shares or payment of dividend to any shareholder, or repayment of any term loan or interest payable thereon to any financial institution or banking company:

Provided that the buy-back is not prohibited, if the default is remedied and a period of three years has lapsed after such default ceased to subsist.

No company shall, directly or indirectly, purchase its own shares or other specified securities in case such company has not complied with the provisions of:

Sections 92: Annual Return

Section 123: Declaration and Payment of Dividend

Section 127: Failure to pay Dividend

Section 129: Failure to give True and Fair Statement.

Buy-back vs Dividend

A dividend offers cash rewards to all shareholders in accordance with their stake in the company, whereas a share buyback returns money only to those who decide to sell their shares. Therefore, paying dividends brings financial benefits even to those who don’t need it right away. When it comes to buy-back, investors have the freedom to decide whether they would like to participate or not. This provides them with the flexibility of altering their respective shareholding structure.

Conclusion:

Choosing between dividends and buy-backs, depends on our personal goals and preferences. If we’re looking to gain regular income from our investment, then dividends may be the preferable choice over buy-back. However, in case of buy-back, investors can decide whether they want to participate in the buy-back process or not. This gives them the option of either holding the shares or change their shareholding portfolio.

WhatsApp

LinkedIn

Pre-Packaged Insolvency Resolution Process (PPIRP) under IBC 2016

September 15, 2024

No Comments

Read More »

SEBI (Delisting of Equity Shares) Regulations, 2021-Imposes new responsibilities on the board of directors.

September 14, 2024

No Comments

Read More »

Summary of Insolvency and Bankruptcy Board of India (Liquidation Process) (Amendment) Regulations, 2024

September 14, 2024

No Comments

Read More »